Rron Rexha is one of the most impressive entrepreneurs I’ve had the opportunity to work with. He just launched his new company Arca with $64 million in funding and more than $1 billion in assets under management. In this podcast discussion, he shares the vision that inspired him to found Arca as an AI-native wealth management platform built around human-first advice. He reflects on his journey from Kosovo to fintech, his year as an Entrepreneur-in-Residence at Venrock, and why he believes the next era of wealth management will be more proactive, personalized, and accessible.

First Arca board meeting: Nick Beim, Jason Wenk, Rron Rexha and Bill McNabb

Rebuilding a services organization bottoms-up with AI can be an extraordinary way to create value, particularly if it means getting rid of legacy technology, creating agentic workflows that enable individuals to focus on their highest-value work and automating almost everything else. What makes the current AI revolution particularly exciting is that new AI capabilities can simultaneously enable step-function changes in the scale and nature of value these organizations can deliver.

Rron Rexha is weaving together all these threads in his new company Arca, which is rethinking wealth management to generate better financial outcomes for consumers, improve the performance of financial advisors and create an organization that is far more efficient and higher-growth than anything the industry has seen. Rron joined us as an Entrepreneur in Residence a few years ago to craft this idea, and he has just launched the company, letting the world know that since starting wealth management operations 7 months ago, the company already manages over $1 billion in customer assets, has raised $64 million and is growing very rapidly.

Importantly, Arca is not seeking to replace financial advisors with AI. I believe that one of the big mistakes Silicon Valley has historically made in wealth management is trying to automate away the financial advisor on the assumption that this is what consumers want, initially with roboadvisors and most recently with AI advisors. In fact, consumers have shown a remarkably strong preference to work with people to help them manage their money for reasons of trust, empathy, understanding and accountability. Roboadvisors were an exciting new innovation, but ultimately became a niche product. There are certainly customer segments where roboadvisors and AI advisors are best-fit products, and these will grow over time, but today they are still small.

What’s revolutionary about Arca is that it is knocking down almost all of the technology the industry is using today and building new capabilities and automation bottoms-up with AI from first principles. This should enable vast improvements in advisor efficiency. Today most advisors spend about 50% of their time stuck in administrative tasks rather than working with clients or growing their business because of the limitations of the existing industry technology stack, which consists of siloed point solutions that communicate poorly with each other. ARCA’s unified technology stack will break down these boundaries, pool all of an advisor’s data, automate most workflows and do much of an advisor’s administrative work, research and analysis in minutes, giving them back most of this time to serve more clients and grow their businesses.

Arca will also make advisors far more effective by bringing world class financial judgment to every contextualized financial decision they make. This will enable optimization of financial planning, portfolio construction and portfolio management to the needs, risk tolerances and tax profiles of their clients to a degree that has not previously been possible. Combined with custom indexing and highly personalized behavioral coaching, this will lead to better financial outcomes for Arca’s customers.

The AI-first approach will create better financial outcomes not only for Arca’s clients, but for its financial advisors, who will be free of the highly limited technology they have to work with today. Working at Arca, they will be able to serve more clients, which provides significant financial upside. They will also be able to deliver better outcomes for these clients, which enables them to expand these relationships and improve retention. A key reason Arca has grown so rapidly is that advisors, who understand the current technological limitations of the industry better than anyone, have expressed a strong preference to work at the company and have voted with their feet to join it.

From a macro perspective, Arca is a building a highly productized form of services organization, where human agents, in this case financial advisors, remain the core of the business, but they are far more efficient and effective because they are empowered by a unified AI foundation that replaces the tangled mess of technology they use today and brings them a much higher degree of financial intelligence than would otherwise be possible.

This should make the company far more scalable, higher-margin and higher-growth than traditional services organizations in wealth management. While existing RIA’s, wirehouses and broker dealer networks can apply AI point solutions on top of their legacy technology stacks, they won’t be able to achieve similar scalability, margins or growth without replacing these stacks altogether, which is very difficult to do, especially for highly-scaled organizations. This type of wholesale rebuild is most effective when it is done from scratch by a small company with an outstanding AI-first engineering team.

Rron has brought together an exceptional group of advisors to help him build the company, including Jason Wenk, the founder and CEO of Altruist; Bill McNabb, the former Chairman and CEO of Vanguard; Morgan Housel, the leading expert on the psychology of money; and Peter Crawford, the former CFO of Charles Schwab.

It’s early days for Arca, but given the advantages in performance, scalability and growth that its AI-first approach confers, I believe it has a lot of ground to take in the wealth management industry in the decades ahead.

(For those who are curious, “arca” comes from Latin and was the holding place for people’s most valuable assets. It’s where heirlooms, money, and documents were kept safe.)

I had a chance to interview Darío Gil about his big new project combining AI, quantum and high-performance computing — the Genesis Mission — and it was incredibly interesting. Darío is one of the most impressive leaders in the quantum industry who previously ran IBM’s research lab and today is the Under Secretary for Science at the U.S. Department of Energy overseeing all 17 national research labs. The Genesis Mission is a new federal initiative that aims to use artificial intelligence and supercomputing to radically accelerate scientific discovery and technological innovation in the United States — to effectively create a “national AI engine” for research. It will develop an integrated AI platform to harness Federal scientific datasets to train scientific foundation models and create AI agents to test new hypotheses, automate research workflows and even conduct experiments. Periodically government-sponsored research produces something extraordinary that has an immense impact on the private sector. I think the Genesis Mission has the opportunity to achieve this.

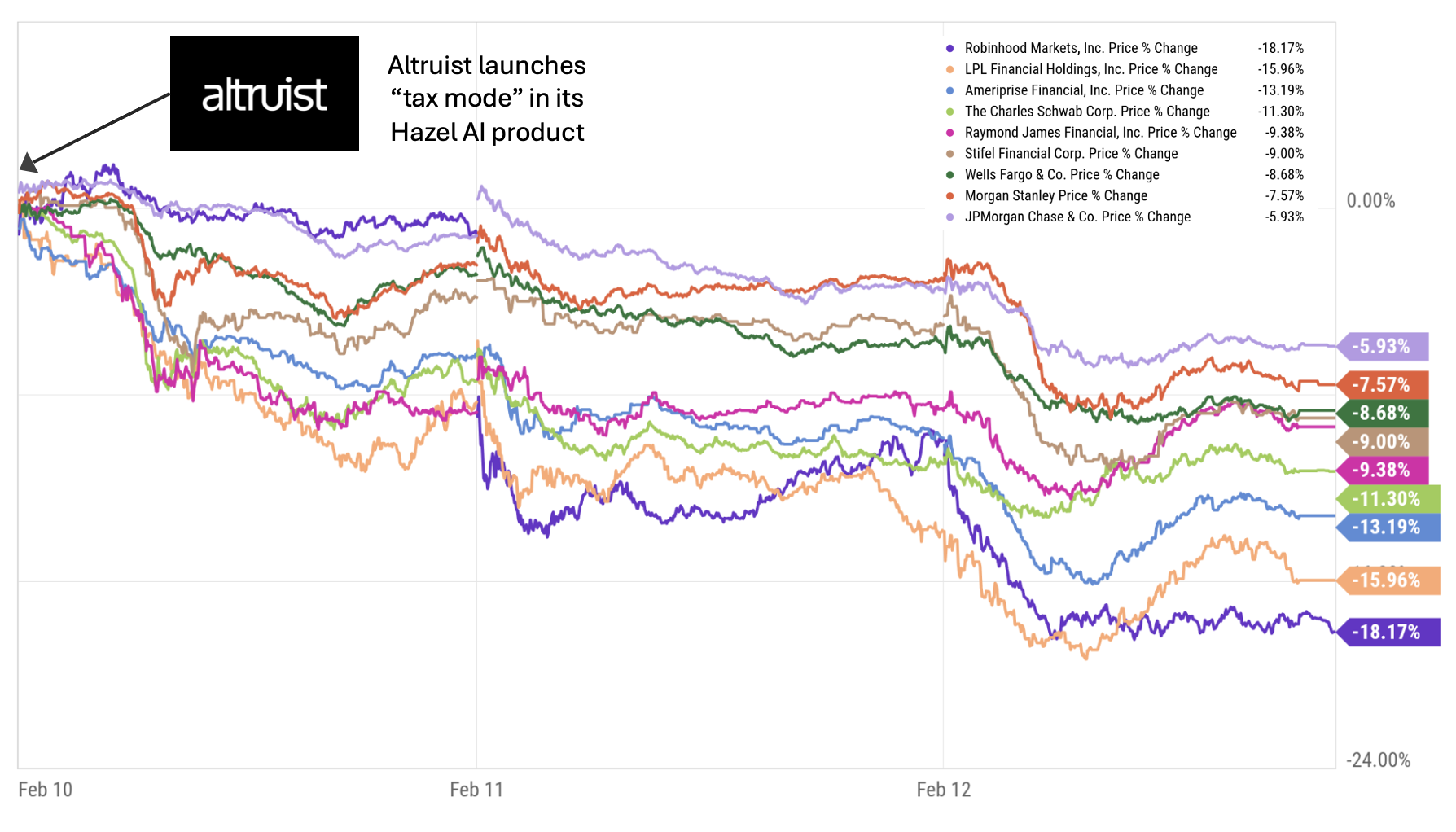

On February 10, Altruist announced a new AI-powered capability called “tax mode” in its Hazel AI product. Public wealth management stocks dropped precipitously, losing $150 billion in value over the next day and a half and leveling off at a total loss of $130 billion by Feb 12. It was wealth management’s DeepSeek moment.

What happened? What is Hazel’s “tax mode”? And what does this episode tell us about how markets are thinking about AI’s impact on wealth management?

What Makes Hazel Different

AI in wealth management is not new. Over the past 18 months, we’ve seen the rise of AI note takers and workflow assistants tailored for financial advisors—companies like Jump and Zocks. These tools sit on top of meetings, generate summaries, pre-fill CRM entries, draft follow-up emails, and help with compliance documentation. They are useful, but not transformational.

Hazel is different for one reason that matters enormously: it is integrated directly into the custodial system and has access to custodial data. Note takers such as Jump and Zocks operate at the “conversation layer.” They hear what the client says. They can summarize goals and generate follow-ups. But they do not have direct, structured, authoritative access to portfolio-level, tax-lot-level, account-level custody data. That means they can’t do things like calculate real-time embedded gains, model tax-loss harvesting across accounts, optimize asset location dynamically and identify wash sale conflicts across household accounts. Hazel can.

Because Altruist is both the advisor’s platform and the custodian, Hazel’s “tax mode” can query the actual ledger of record. It can look at every lot, every gain, every loss, every account registration. It can move from conversation to action without manual reconciliation between systems. That’s a fundamentally different starting point than an AI tool that only listens to a Zoom call.

Why Tax Is the Most Valuable—and Most Difficult to Scale—Service in Wealth Management

In wealth management, advisors often say that tax alpha is the most tangible value they create. Investment returns are partly market-driven. Behavioral coaching is real but hard to quantify. Planning is episodic. But tax management—done correctly—can produce measurable, after-tax outperformance year after year.

And yet, tax optimization is one of the hardest services to scale. Why? Because it involves painstaking research and analysis involving cross-account coordination, household-level modeling, timing sensitivity, compliance and documentation, and because it requires advisor judgment.

Today, many advisors still rely on spreadsheets, manual analysis and fragmented tools to deliver tax insights. Even with modern rebalancing software, true household-level, dynamic, AI-driven tax optimization remains complex and labor-intensive.

Hazel’s “tax mode” attacks exactly this bottleneck. It can instantly surface tax-loss harvesting opportunities, simulate gain-offset strategies, optimize asset location across taxable and tax-deferred accounts and draft client-ready explanations in seconds.

In other words, it converts high-skill, low-scale labor into software leverage. That’s why the market reacted.

Why Existing Custodians Are at a Structural Disadvantage

It would be easy to assume that large custodians like Charles Schwab or Fidelity could simply replicate Hazel’s functionality. But that assumption overlooks something structural: legacy custody platforms are not modern wealth infrastructure. Most large custodians operate on decades-old systems layered with multiple acquired platforms, patchwork integrations, batch-processing architectures, rigid data schemas and complex internal permissioning systems. These systems were not built for real-time AI integration. They were built for record-keeping, trade settlement, regulatory reporting and operational stability.

To integrate a true AI tax engine at the core of custody requires clean and normalized data architecture, real-time API access, flexible permissions and modular service design. Altruist, as a modern fintech custodian built in the cloud era, has the architectural advantage. Its custody stack was built with modern technology, APIs and data-layer accessibility in mind. By contrast, retrofitting AI deeply into a legacy custody core is more like open-heart surgery than adding a feature.

This doesn’t mean Schwab or Fidelity won’t respond. It means the speed and depth of response are structurally constrained. Markets are extremely sensitive to that distinction.

Why the Market Reaction Was So Large

The selloff was not just about tax-loss harvesting software. It was about the potential repricing of advisor productivity, platform differentiation, margin structures, custody defensibility and client acquisition economics.

If AI tools embedded in modern custodians materially increase advisor productivity, several second-order effects follow:

Advisors may consolidate onto AI-enabled platforms

Smaller RIAs could scale faster with fewer staff

Tax alpha becomes more standardized

Client expectations rise

Platform switching becomes more attractive

For firms that earn basis points on trillions of AUM, even a small change in retention, growth, or pricing power compounds dramatically.

Markets price optionality. And they price competitive displacement risk even more aggressively.

One Interpretation: How Much Value Could AI Create?

One way to interpret the $130 billion market drop is not as a measure of value destroyed, but as a real-time, market-implied estimate of potential value transfer in the industry.

Consider:

The U.S. wealth management industry oversees roughly $30–40 trillion in advised assets

Advisors typically charge 50–100 basis points

Even a 5–10 basis point shift in value capture (through better tax optimization, other new AI capabilities and competitive pressure) equates to tens of billions annually

Who captures this value? Advisors themselves seem well-positioned to capture some of it. If AI-enabled tax optimization allows them to deliver 20–40 basis points of after-tax alpha, or reduce staffing costs by 20–30%, or improve client retention by even 1–2%, the cumulative value creation across the industry could be significant.

Consumers themselves will benefit greatly from faster, more automated and more rigorous tax optimization and other AI capabilities to come. And some advisors offering leaner, more responsive organizations may choose to share some of these gains in the form of lower fees.

One significant set of beneficiaries of this value transfer will be providers of powerful new AI capabilities that are not easily replicated by others. Altruist is off to a strong start in this category as a high-tech, full-stack custodian with a growing suite of AI-enabled capabilities embedded in its Hazel platform. It has already announced additional Hazel modules for financial planning and compliance support to be released in the quarters ahead, and many more will follow.

At Venrock we have invested in a variety of AI-enabled technology companies in wealth management seeking to provide similarly high-value products and services that cannot be easily replicated. In addition to Altruist, these include FINNY (an AI-enabled prospecting platform for advisors with its own data infrastructure), Moment (a fixed income trading and portfolio management platform with its own data and execution infrastructure), Vanilla (AI-enabled estate planning software) and two additional companies that will come out of stealth mode shortly.

The Big Picture

The wealth management industry has historically been insulated from software-style disruption because of some of the core characteristics of advisory work: relationships matter, regulation slows change and switching costs are real.

AI doesn’t eliminate these factors. But it does amplify the advantages of modern infrastructure. Hazel’s significance is not just that it uses AI. It is that it uses AI at the custodial data layer, enabling tax optimization—and ultimately additional capabilities—to be delivered programmatically. That’s why other AI note takers cannot replicate it. That’s why legacy custodians face integration challenges. And that’s why markets erased over $130 billion in market value in days.

The episode suggests something larger: AI’s value in wealth management will not come from replacing advisors, but from radically increasing their leverage. And in a trillion-dollar industry built on basis points and operating leverage, even modest improvements in productivity, tax alpha, and platform differentiation can justify very large valuation swings.

The market reaction may ultimately prove exaggerated. But it revealed something unmistakable: investors believe AI can reshape the economics of wealth management at scale. And when the ledger of record meets the language model, the consequences ripple far beyond a single product announcement.

I had an opportunity to speak with David Weisburd on what happens when general intelligence commoditizes, the promise of vertical AI and the impact of AI in wealth management and defense. We also had chance to discuss what I think is one of the most interesting cognitive bias traps in venture investing, which is when pattern recognition – which helps you sift through 95% of investment opportunities with extraordinary efficiency – utterly fails you when it comes to some of the most successful venture investments. Love how they digitally dressed me in a tie for the cover photo :). You can listen to the discussion here.